Premium increases in private health insurance (private Krankenversicherung or short PKV) are a recurring topic that concerns many policyholders every year. However, some insurers and tariffs are affected more than others, depending on the specific benefits covered. It is therefore advisable to consider options such as switching tariffs or adjusting your deductible to keep costs manageable.

Everything You Need to Know About PKV Premium Increases

Premium adjustments in private health insurance are caused by a combination of factors: medical progress, longer life expectancy, lower returns on capital reserves, and the need to align premiums with actual healthcare expenses when these exceed the calculated costs.

To counter rising premiums in private health insurance, you can either switch to another tariff within your current insurer, change to a different provider, or adjust the scope of your existing plan.

Over the past 20 years, premiums in the statutory health insurance system (GKV) have tended to rise more frequently and sharply than in private health insurance. PKV premium increases occur less often but are typically more noticeable when they happen.

Premiums in private health insurance are not raised arbitrarily. Increases are strictly regulated by law and must be reviewed by independent trustees. Adjustments are only initiated when actual healthcare costs or mortality rates exceed a certain threshold (usually 5–10%) and the deviation is not temporary.

Why Do Private Health Insurance Premiums Rise?

Medical Progress and Healthcare Costs

One key factor is medical inflation. New treatments and advanced technologies improve healthcare but also drive up treatment costs. Rising prices for medical services, medications, or hospital stays directly impact the calculation of premiums.

Longer Life Expectancy

Longer life expectancy also plays a crucial role: as people live longer and use medical services for more years, insurers must build sufficient reserves to offset these increasing long-term costs.

Actuarial Interest Rate (Rechnungszins)

The actuarial interest rate is another influencing factor — it represents the assumed return insurers expect to earn on invested premiums. If actual investment returns fall short of expectations, insurers must lower the actuarial interest rate during the next premium adjustment — and compensate for it with higher premiums.

Adjustment to Actual Benefit Expenses

Another major reason for premium increases is aligning with actual healthcare expenses.

When the insurer’s real expenditure on medical services exceeds the calculated costs by a specific threshold (typically 5–10%, depending on the policy), the insurer is required by law to adjust premiums. Once the deviation exceeds 10%, a premium adjustment becomes mandatory.

This ensures that the insurer’s revenue is sufficient to cover higher healthcare costs.

What You Can Do About High Premiums

Switch to Another Tariff Within Your Current Insurer

Switching tariffs internally within your private health insurance can effectively reduce your premiums without losing essential benefits. According to the German Insurance Contract Act (VVG), every privately insured person has the right to change to another tariff within the same insurance company.

If the new tariff offers equivalent or fewer benefits, you can switch without another health check. Even older policyholders or those with pre-existing conditions can often achieve significant savings this way — sometimes several hundred euros per year — without losing important coverage.

A new health check is only required if you upgrade to a tariff with more extensive benefits.

Another advantage: an internal tariff change is possible at any time and is not bound to fixed deadlines. Additionally, all accumulated aging reserves are transferred to the new tariff.

Note: Some insurers may have specific timing rules, such as the main renewal date, the next possible cancellation date, or the first day of the following month with one month’s notice.

Switching to Another Insurer

If your private health insurer has increased your premiums again, you might be considering changing providers. Under certain conditions, switching can be worthwhile — especially if you’re still young and haven’t yet built up significant aging reserves. However, this decision should be carefully weighed.

Switching insurers involves a new health check, where pre-existing conditions can lead to surcharges or even rejection. In addition, accumulated aging reserves can’t always be fully transferred. For contracts concluded before 2009, transfer is not possible at all.

That’s why it’s important not to rush this decision. A detailed consultation can help you find the best option for your individual situation — allowing you to benefit from a stable and fair premium in the long term without compromising on benefits.

Reducing Benefits or Increasing the Deductible

Another way to lower your premiums is to adjust your existing tariff. You can reduce the range of benefits — for example, by removing optional services — or choose a plan with a higher deductible.

A higher deductible means you’ll cover a larger share of annual treatment costs before your PKV starts paying, but your monthly premiums will decrease noticeably.

As long as you switch to a plan with equal or fewer benefits, no new health check is required. The same applies to increasing your deductible, as long as you don’t add new benefits. Your accumulated aging reserves also remain intact.

Think carefully about which benefits are truly essential to you and what level of deductible you can comfortably afford.

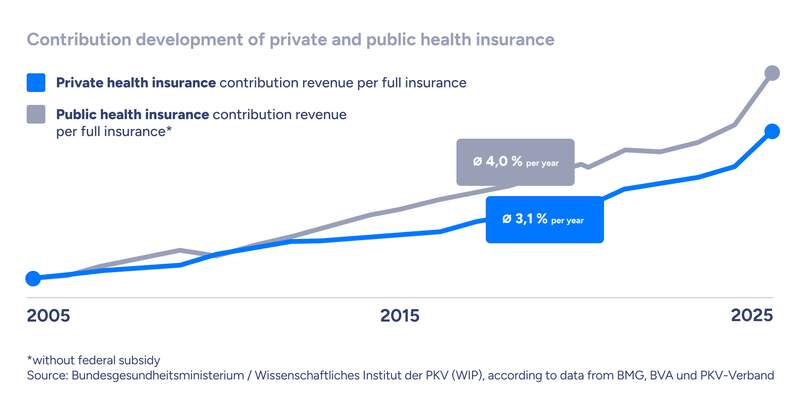

“Both public and private health insurance premiums increase over time — for example, due to medical progress or longer life expectancy. However, unlike public insurance, private insurers cannot simply cut promised benefits. What you are contractually guaranteed remains in place. While public insurance premiums are based on income, private premiums are determined by your personal factors at the time of enrollment. And the data shows: since 2005, public health insurance contributions have actually risen faster than private ones.”

Lukas HärleKey Account Manager

Comparing Premium Increases: PKV vs. GKV

In practice, statutory health insurance premiums (GKV) have risen more sharply over the past 20 years than private ones, mainly due to rising healthcare costs and demographic changes.

Public health insurers have implemented almost annual premium increases in recent years, while private insurers typically adjust premiums less frequently but more noticeably.

A comparison chart illustrates how premiums have developed over the past two decades.

Statistics: Premium Increases in Public and Private Health Insurance Over Time

When Do PKV Premiums Increase?

Private insurers cannot raise premiums arbitrarily. Adjustments are subject to strict legal regulations and must be verified by independent trustees. Only when healthcare costs exceed a defined threshold is a recalculation initiated.

If actual costs surpass projected expenses by 5–10% (depending on the tariff), private insurers are legally required to review their premiums. Adjustments are only made when the deviation is not temporary. Similarly, if mortality rates differ by more than 5%, an adjustment becomes necessary.

The final review of any premium adjustment is carried out by an independent trustee, ensuring that the increase is justified and compliant with regulations.

Finally, the Federal Financial Supervisory Authority (BaFin) is informed. If no objection is raised, the premium adjustment (BAP) can proceed. If the justification is insufficient or flawed, the increase may even be deemed invalid.

FAQs About PKV Premium Increases

Private health insurers can adjust premiums once per year — but only if certain conditions are met. An increase is allowed when actual healthcare costs significantly exceed the projected expenses. Once this threshold is reached, the insurer may adjust premiums to maintain the tariff’s long-term financial stability. If your premium is raised, you have a special right of termination: you can cancel the policy within two months after receiving the adjustment notice.

You cannot directly object to a premium increase, as it is based on contractual and legal foundations. Adjustments are calculated according to defined criteria and reviewed by an independent trustee. As long as the increase is properly justified and approved, it is legally binding.

When premiums increase, private insurers receive more income — but this is primarily used to secure policyholders’ long-term financial stability.

A significant portion flows into aging reserves, which help offset rising healthcare costs in old age and stabilize premiums. Additional funds are also needed to cover higher medical expenses, new treatments, and increased healthcare provider fees.

Regular recalculations ensure that promised benefits remain financially sustainable, so private insurers can continue to offer reliable and high-quality medical care to their members.

Premium increases usually take effect on January 1 or July 1 each year. Policyholders must be informed at least one month in advance through a written notice that explains the reasons and legal basis for the adjustment.

WRITTEN BYottonova Magazin Autor:in

Weitere Artikel

Hi!

Unfortunately our chat is currently closed.

But you can also just leave your request here and we'll get in touch with you as soon as possible!

Form successfully submitted!

Sorry, a problem has occurred. Please try again later.

Vielen Dank!

Deine E-Mail-Adresse wurde erfolgreich bestätigt.

Thank you

You have successfully confirmed

your appointment.

Your appointment reservation has expired

Would you like to book a new appointment instead?

Thank you

You have successfully confirmed

your email address.

Unsubscribed successfully!

You have been unsubscribed from our newsletter.

Consent declaration

By entering your data you agree to be contacted by ottonova via phone, SMS and email. Good to know:

We use your data exclusively to consult and inform you about ottonova health insurance products.

You can revoke your consent to be contacted at any time. To do so, please send an email to support@ottonova.de.

Further information on how we handle data privacy can be found in our data privacy statement.

We will call you soon.

You have already booked an appointment with us. We will contact you on the following date/time. See you soon!

Thank you.

Please check your email inbox to confirm your appointment

on

at

.

Please check your email inbox to confirm your email address.

We need your consent to show this YouTube video

This content is not permitted to load due to trackers that are not disclosed to the visitor. The website owner needs to setup the site with their CMP to add this content to the list of technologies used.

Accessibility at ottonova

At ottonova, we strive to make our website as accessible as possible. Therefore, please use accessibility@ottonova.de exclusively for suggestions and comments regarding accessibility on the website.

Are you already insured with ottonova and have another issue? Please log in to the web app and contact us there.

Please only share sensitive data such as health information in your secure area within the app or web app.

If you are not yet insured with us and have questions about our insurance products, please feel free to contact us via chat or email.

Callback

Get a consultation

Callback

Get a consultation

+49 89 121 896 09

Talk to an expert

+49 89 121 896 09

Talk to an expert